Do you ever wonder why your savings account isn’t growing as fast as you’d hoped? Or perhaps you’ve noticed that maintaining a certain balance is crucial to avoid pesky fees? Understanding the typical minimum balance required for traditional savings accounts is key to managing your finances effectively.

Whether you’re just starting out with saving, managing a household budget, or planning for long-term financial goals, knowing this information can save you from unnecessary charges and help you make smarter financial decisions.

In this blog, we'll break down what a minimum balance is, why it matters, and who should be particularly mindful of it.

What is a Traditional Savings Account?

A traditional savings account is one of the most common types of bank accounts designed for individuals looking to store their money securely while earning a modest interest over time.

Unlike checking accounts, which are primarily used for daily transactions, a traditional savings account is intended for longer-term savings and often comes with restrictions on the number of withdrawals you can make each month.

These accounts are typically offered by banks and credit unions and are insured by the FDIC or NCUA, making them a safe place to keep your funds. Ideal for building an emergency fund or saving for future goals, a traditional savings account offers both security and accessibility, making it a foundational element in any personal financial plan.

Types of Traditional Savings Account

When it comes to traditional savings accounts, not all are created equal. Different types cater to varying financial needs, offering distinct features and benefits. Understanding these variations can help you choose the right account for your savings goals.

Here are the main types of traditional savings accounts:

- Basic Savings Account: Offers easy access to your money with minimal fees but typically provides the lowest interest rates.

- High-Yield Savings Account: Provides a higher interest rate compared to basic accounts but may require a higher minimum balance.

- Student Savings Account: Designed for students with low or no minimum balance requirements, often with no monthly fees.

- Joint Savings Account: Allows multiple individuals to co-own the account, making it ideal for couples or families.

- Custodial Savings Account: Managed by an adult for the benefit of a minor, useful for building savings for a child’s future.

How Does a Traditional Savings Account Work?

A traditional savings account operates by allowing you to deposit money that earns interest over time, making it a safe and reliable option for growing your savings. However, to maintain this account, banks often require you to keep a minimum balance, typically ranging from $300 to $500.

Falling below this threshold could result in a monthly service fee, which usually amounts to around $5. This means that to maximize the benefits of your savings account, you need to be mindful of maintaining the required balance, thereby avoiding unnecessary fees that could erode your savings over time.

What is the Typical Minimum Balance for a Traditional Savings Account?

The typical minimum balance for a traditional savings account varies by account type and financial institution. This balance is the minimum amount you need to maintain in your account to avoid monthly fees. For basic savings accounts, the required balance typically ranges from $300 to $500.

However, accounts offering higher interest rates or online accounts might have different requirements, sometimes higher or even no minimum balance. Understanding these thresholds is essential to avoid unnecessary fees and optimize your savings potential.

Minimum Balances for Basic Savings Accounts

Basic savings accounts generally have lower minimum balance requirements and come with modest interest rates. Below is a comparison of the minimum balance requirements and fees from some well-known U.S. banks:

| Bank | Minimum Opening Deposit | Required Ongoing Balance | Monthly Fee if Requirement Not Met | Alternative Ways to Avoid Fees |

| Wells Fargo (Way2Save) | $25 | $300 daily balance | $5 | Waived if you set up automatic transfers of at least $25 or $1 daily from a linked Wells Fargo checking account, or if the primary account holder is under 25. |

| Chase (Chase Savings) | $0 | $300 daily balance | $5 | Waived for account holders under 18, or with automatic transfers of $25 from a Chase checking account, or with other linked Chase accounts. |

| Bank of America (Advantage Savings) | $100 | $500 daily balance | $8 | Avoid fees by linking to a Bank of America Advantage Relationship account, becoming a Preferred Rewards member, or being under 25 and a student. |

| Citi (Basic/Access Savings) | $0 | $500 average monthly balance | $4.50 | No additional fee waivers. |

| U.S. Bank (Standard Savings) | $25 | $300 daily or $1,000 average balance | $4 | Waived for account holders under 18 years old. |

| Citizens Bank (One Deposit Savings) | Any amount | $200 daily balance | $4.99 | Waived for those under 25 or over 65, or with at least one deposit per month. |

| Fifth Third (Traditional Savings) | $0 | $500 average monthly balance | $5 | Waived with a Fifth Third checking account, for account holders under 18, or with military banking enrollment. |

| PNC (Standard Savings) | $25 (or $0 if opened online) | $300 average monthly balance | $5 | Waived with a linked PNC checking account, for account holders under 18, or with automatic monthly transfers of $25. |

| TD Bank (TD Simple Savings) | $0 | $300 daily balance | $5 | Waived for account holders 18 and under, or 62 and older. |

Minimum Balances for High-Interest Accounts

High-interest savings accounts generally require higher balances but offer better interest rates. Here’s a breakdown of the requirements:

| Bank | Minimum Opening Deposit | Ongoing Balance Requirement | Monthly Fee if Requirement Not Met | Other Fee Waivers |

| Wells Fargo (Platinum Savings) | $25 | $3,500 daily balance | $12 | No additional waivers available. |

| Chase (Premier Savings) | $0 | $15,000 daily balance | $25 | Waived with a linked Premier Plus Checking or Sapphire Checking account. |

| Citi (Priority Package) | $0 | $50,000 average balance | $30 | No additional waivers available. |

| Citizens Bank (Quest Savings) | Any amount | $0 balance | $0 | Fee waived if linked to a Citizens Quest Checking account. |

| TD Bank (Beyond Savings) | $0 | $20,000 daily balance | $15 | No additional waivers available. |

Minimum Balances for Online Accounts

Online savings accounts often offer lower or no minimum balance requirements, along with fewer fees. Here’s how they compare:

| Bank | Minimum Opening Deposit | Ongoing Balance Requirement | Monthly Fee if Requirement Not Met | Other Fee Waivers |

| Smarty Pig by Sallie Mae | $0 | $0 | $0 | No monthly fees applicable. |

| Affirm | $0 | $0 | $0 | No monthly fees applicable. |

| Ivy Bank | $2,500 | $2,500 for the highest APY | 0.05% APY | No additional fee waivers available. |

| Axos Bank | $250 | $0 | $0 | No monthly fees applicable. |

| Alliant | $5 | $100 average daily balance | None | $1 paper statement fee waived with electronic statements. |

| Truist Online Savings | $0 | $0 | $0 | Monthly fee waived with a $25 preauthorized internal transfer. |

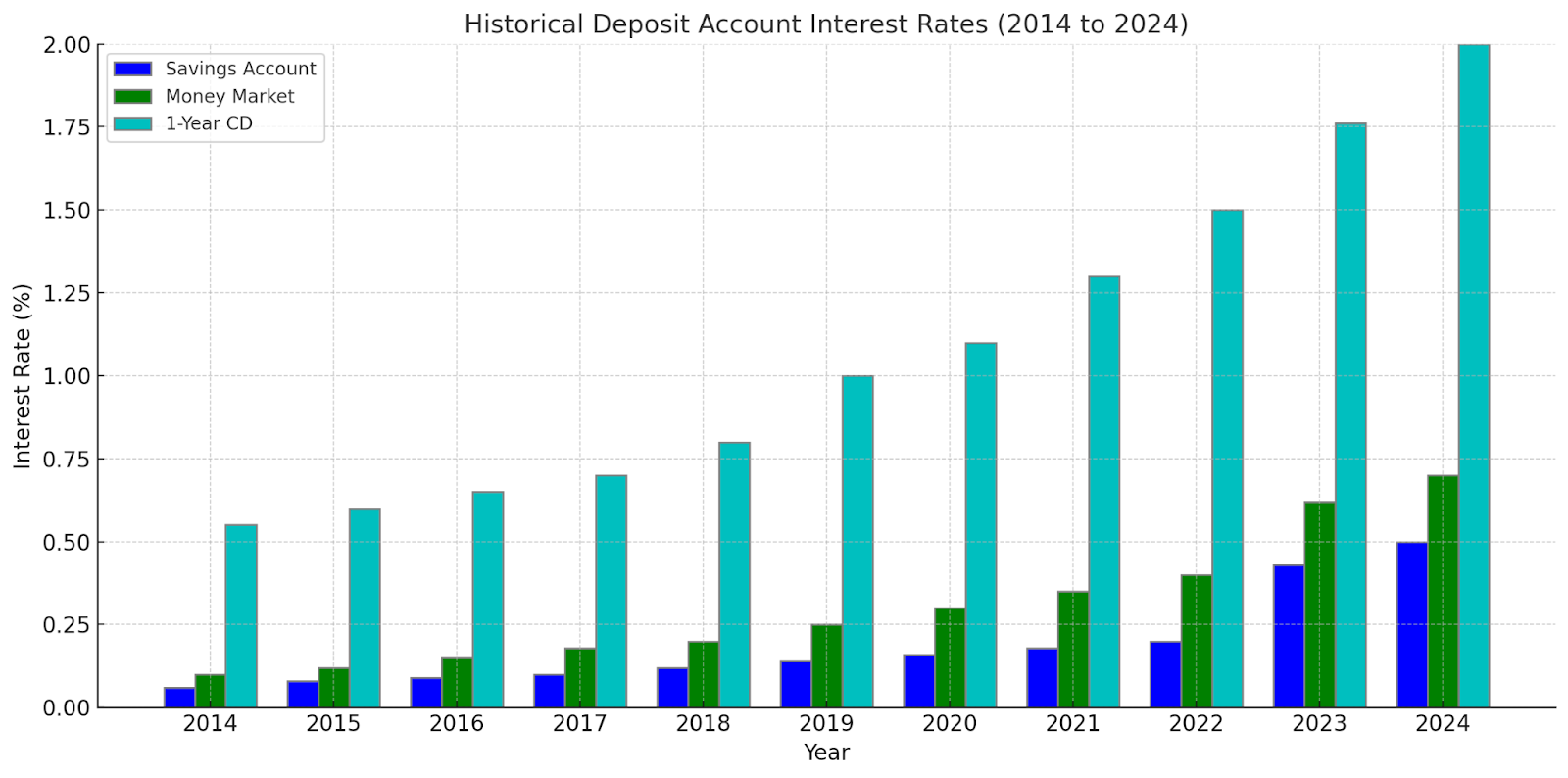

Traditional Savings Account Typical Interest Rate

Traditional savings accounts are a popular choice for individuals looking to save money with minimal risk. However, they typically offer lower interest rates compared to other savings vehicles like money market accounts or certificates of deposit (CDs).

The interest on a savings account is expressed as the Annual Percentage Yield (APY), which reflects the actual rate of return on your deposit over a year, accounting for compounding interest. While these rates have been relatively low over the past decade, they have been slowly rising in recent years.

For instance, the national average savings account rate is currently around 0.43%, significantly lower than the 0.62% offered by money market accounts and the 1.76% provided by 1-year CDs.

Pros and Cons of a Traditional Savings Account

A traditional savings account is one of the most straightforward and accessible financial products available, offering both benefits and drawbacks depending on your financial goals. Understanding these pros and cons can help you decide whether this type of account is the right fit for your needs.

Pros:

- Security: Traditional savings accounts are typically insured by the FDIC (Federal Deposit Insurance Corporation) up to $250,000, providing peace of mind that your money is safe.

- Liquidity: Your funds are easily accessible, allowing you to withdraw or transfer money quickly in case of emergencies.

- Simplicity: These accounts are easy to open and manage, making them an ideal option for individuals who prefer a straightforward approach to saving.

- No Risk of Loss: Unlike investments in the stock market or other volatile assets, the principal amount in a savings account is not subject to market fluctuations.

Cons:

- Low Interest Rates: The interest rates on traditional savings accounts are often lower than other savings vehicles, meaning your money grows more slowly over time.

- Inflation Risk: Because the interest earned may not keep pace with inflation, the purchasing power of your money could decrease over time.

- Fees: Some banks charge monthly maintenance fees if you don't maintain a minimum balance, which can erode your savings.

- Limited Growth Potential: With lower returns compared to other investment options, a traditional savings account may not be the best choice for long-term wealth accumulation.

Closing Note

By maintaining the required balance, you can avoid unnecessary fees and ensure that your savings grow over time. While traditional savings accounts offer security and easy access to your funds, it's important to be aware of the limitations, such as low interest rates and potential fees. Weighing the pros and cons will help you decide if this type of account aligns with your financial goals, ensuring you make the most out of your savings.