When it comes to managing your business's financial health, understanding depreciation is key. One method that often stands out, especially for small businesses, is the Double Declining Balance (DDB) Method. But what exactly is it, and why should you care?

Unlike straight-line depreciation, which spreads the cost of an asset evenly over its useful life, the DDB method accelerates depreciation, reducing an asset's book value much faster in the early years.

Whether you're a startup looking to maximize your deductions or a growing business fine-tuning your financial strategy, understanding how this method works can make a significant difference to your bottom line.

What is Depreciation?

Depreciation is the accounting process used to allocate the cost of a tangible asset over its useful life. It reflects the gradual wear and tear, decay, or obsolescence of an asset as it ages. Whether it’s machinery, vehicles, or office equipment, every physical asset loses value over time.

Depreciation helps businesses record this decline on their financial statements, providing a clearer picture of the actual value of their assets at any given time.

It also serves as an essential tool for calculating tax deductions, allowing businesses to spread out the cost of high-value purchases over multiple years.

Why Use the Double Declining Balance Method?

The Double Declining Balance (DDB) method is a form of accelerated depreciation that allows businesses to write off more of an asset's value in the earlier years of its life. This method is particularly beneficial for assets that lose their functionality or value faster in the beginning, like technology or machinery.

By using DDB, businesses can match higher depreciation expenses with periods of higher revenue, optimizing tax benefits and improving cash flow during crucial growth phases.

- Accelerates depreciation for faster write-offs

- Ideal for assets that lose value quickly

- Increases tax deductions in early years

- Aligns expenses with higher revenue periods

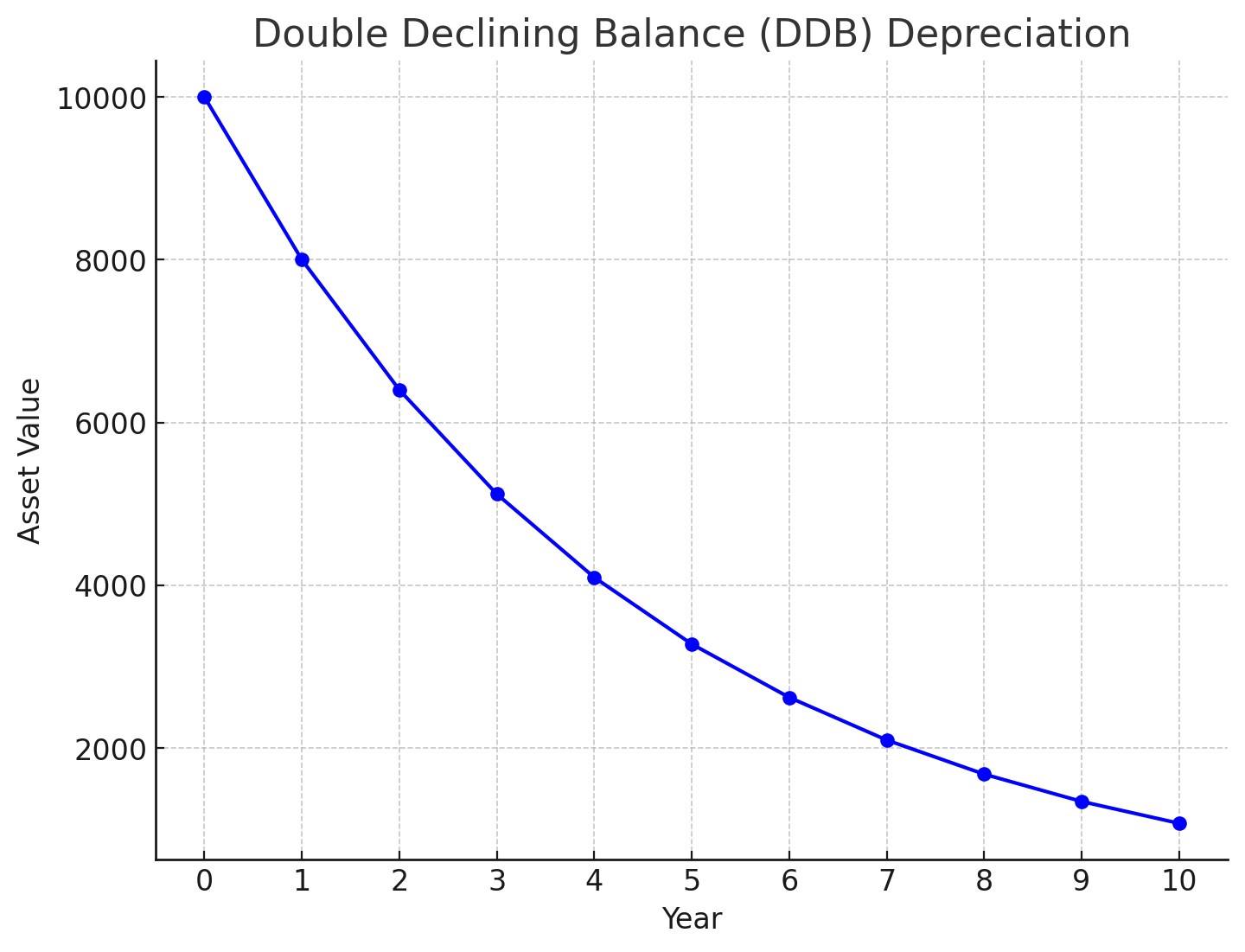

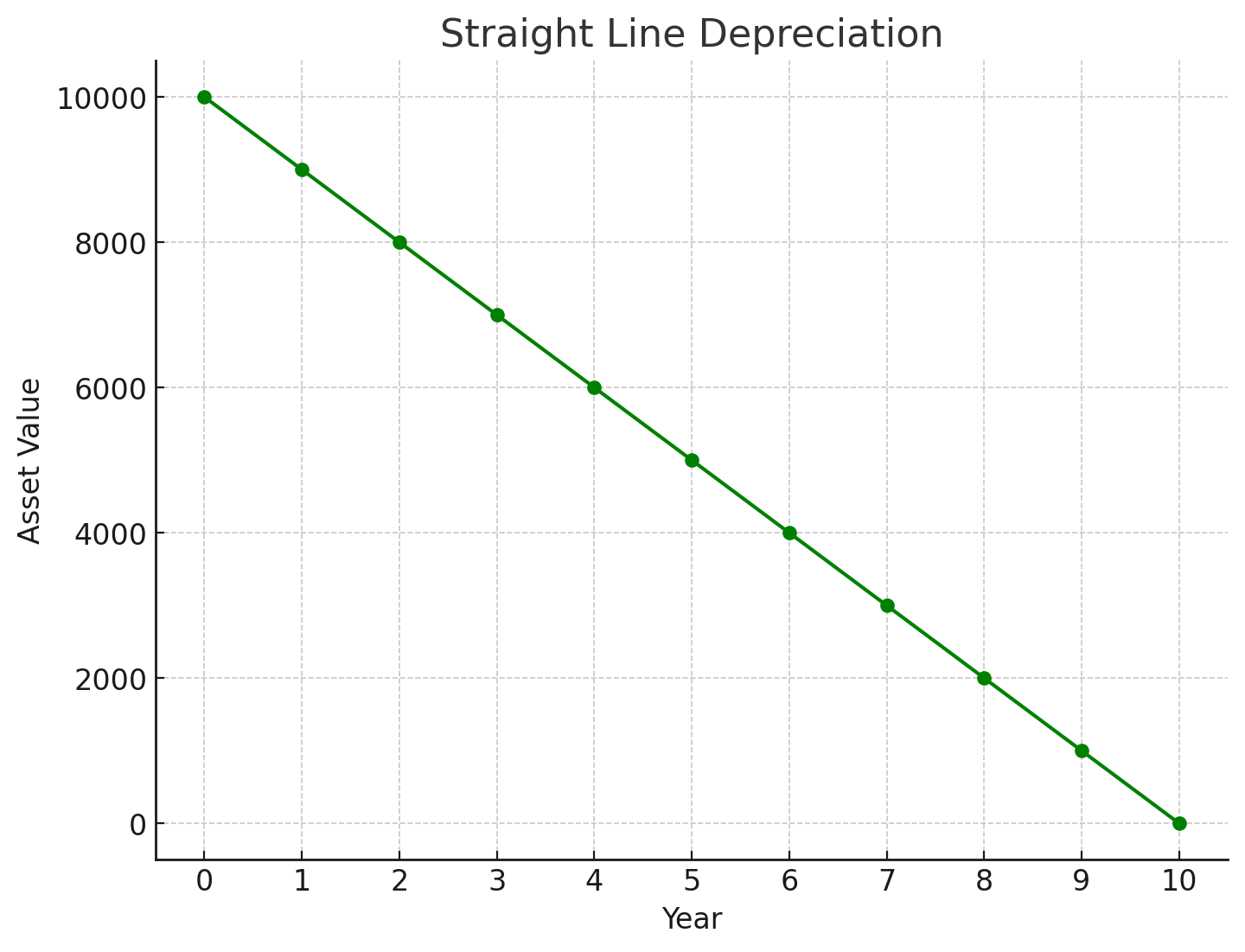

Double Declining Balance vs. the Straight Line Method

The DDB method allows businesses to write off a larger portion of an asset’s value in its early years. This accelerated depreciation method is ideal for assets that lose value quickly, like machinery or technology.

On the other hand, the Straight Line method spreads depreciation evenly across the asset’s useful life. It's simple and predictable, ideal for assets that decline steadily, such as furniture or buildings.

Formula for Double Declining Balance Depreciation

The Double Declining Balance (DDB) method calculates depreciation by applying a constant depreciation rate, which is double the rate of the straight-line method, to the asset's book value at the beginning of each year. This approach accelerates depreciation in the early years of the asset’s life, resulting in larger deductions upfront.

Formula:

Depreciation Expense = 2 × ( 1/Useful Life of Asset ) × Book Value at Beginning of Year

When to Use the Double Declining Balance Method?

The Double Declining Balance method is most effective when you have assets that lose value quickly or become obsolete early in their lifespan, such as technology, vehicles, or manufacturing equipment.

Businesses often use this method when they want to accelerate tax deductions in the early years of an asset’s life, maximizing upfront cash flow. This method is also suitable when an asset is expected to generate more revenue in its initial years, allowing depreciation expenses to better match income during this period.

It’s especially beneficial for businesses looking to reinvest in growth by freeing up capital sooner.

Example of the double declining balance method

Imagine a business purchases office equipment for $10,000 with a useful life of 5 years. Using the Double Declining Balance method, the depreciation rate is calculated as:

Double Declining Balance method, the depreciation rate is calculated as:

Depreciation Rate = 2 × ( 1/5 ) = 40%

In the first year, the depreciation expense would be:

Depreciation = 40% × 10,000 = 4,000

So, after the first year, the book value would be:

10,000 − 4,000 = 6,000

In the second year, the depreciation is applied to the new book value:

Depreciation = 40% × 6,000 = 2,400

After the second year, the new book value would be:

6,000 − 2,400 = 3,600

This process continues each year until the asset is fully depreciated.

Example 2: Depreciating a Vehicle

A business buys a delivery vehicle for $20,000 with a useful life of 4 years. Using the Double Declining Balance method, the depreciation rate would be:

Depreciation Rate = 2 × ( 1/4 ) = 50%

In the first year, the depreciation expense is:

Depreciation = 50% × 20,000 = 10,000

So, the book value at the end of the first year is:

20,000 − 10,000 = 10,000

In the second year, the depreciation would be:

Depreciation = 50% × 10,000 = 5,000

After the second year, the book value becomes:

10,000 − 5,000 = 5,000

The vehicle's value continues to decrease, with lower depreciation amounts each year.

Conclusion

The Double Declining Balance Method is a valuable tool for businesses looking to accelerate depreciation and maximize tax benefits in the early years of an asset's life. By applying a higher depreciation rate upfront, this method allows businesses to better match expenses with revenue, improve cash flow, and more accurately reflect the declining value of assets like machinery, technology, or vehicles. For companies focused on growth or reinvestment, the DDB method offers a strategic advantage in financial planning.